Dividends Don't Drive Total Return They Contribute To It: Part 1

Every investor would be wise to know where and how long-term returns are generated.

There are two primary sources of common stock returns.

Dividends contribute to returns, but they are not a source.

Introduction

I believe there is a critical piece of investment wisdom that all investors in common stocks should possess. Every common stock investor should have a clear understanding of where and how long-term common stock returns are generated or come from. When an investor does not possess this knowledge, they can be easily led towards drawing erroneous conclusions about their portfolios and/or the individual stocks that they own. Knowledge is power, and the knowledge of where and how long-term stock returns are generated is incredibly enlightening.

Importantly, every common stock investor should also understand that there are significant differences regarding how or where short-term stock returns come from or are generated. In the short run, common stock prices can go anywhere, often do, and often defy logic in the process. Therefore, when dealing with the short run, it's critical to recognize anomalous price behavior when it is manifest. This empowers the prudent and intelligent common stock investor in making sound long-term investment decisions. However, don't confuse sound decisions with short-term market timing decisions. The first is prudence in action, and the latter is merely guessing.

The Primary Sources or Drivers of Long-Term Returns When Investing in Common Stocks

There are two primary sources or drivers of long-term returns when investing in common stocks. The first, and fundamentally the most important, is the rate of change of earnings growth (and/or cash flow growth) that the business behind the stock generates. Simply stated, the faster a business grows its earnings and cash flows, the greater the long-term returns it will generate for its stakeholders over the long run. Stated differently, all things being equal, a faster growing business will generate greater long-term returns than a slower growing business. Long-term investment returns are functionally related to how fast a company grows its business.

The second primary source is the valuation (not the price) you pay to buy a company's earnings growth (and/or cash flow growth). Too high of a valuation will cause you to earn less than the company's growth warrants, and a low valuation will cause you to earn more than the company's growth warrants. And just like the porridge in the fairytale Goldilocks and the Three Bears, when you get valuation just right, your long-term returns will be highly correlated to the company's earnings growth (and/or cash flow growth) rate achievements.

However, in addition to these primary sources or drivers of return, there are also contributors, or contributing factors. The most common or obvious contributor to long-term returns are dividends, if a company pays one. The reason I suggest that dividends are a contributor rather than a source of long-term returns, is simply because dividends are paid out of earnings (or cash flows) which as stated above is the primary source. Moreover, the total amount of dividends (if any), as well as the long-term growth of dividends are also directly related to the growth of earnings (or cash flows).

The consistency of the company's earnings growth (and/or cash flow growth) is another important contributor to long-term returns. The long-term returns produced by a cyclical company can vary greatly from one cycle to the next. In other words, if you are measuring long-term returns at the bottom of the cycle, they can be significantly less than they would be if you measure them at the top of the cycle. However, once again, the primary source remains the earnings (or cash flow) growth. At the bottom of the cycle earnings growth (and/or cash flow growth) will likely average low, while at the top of the cycle earnings growth (and/or cash flow growth) will average higher.

The Total Return VS Dividends Debate: A Classic Case of Erroneous Conclusions

My inspiration for writing this article came as a result of a recent article written by fellow Seeking Alpha contributor Psycho Analyst titled "This Total Return Vs. Dividends Smack Down Between 13 Top Dividend Aristocrat Survivors Will Wake You Up."

I found the article interesting, and generally well-written, and the calculations accurate as presented. However, I have a specific reason for citing this article here in my work. I was not specifically referenced in the article, but I was prominently mentioned several times in the comment thread that followed, including a comment by the author. It was that comment that served as my primary inspiration which I present in its entirety as follows:

"Psycho Analyst

Rick,

For me, the most interesting thing to emerge out of the data was how large the range was of total return in a group of stocks that are perceived by many as having very similar characteristics.

Chuck's approach seems to be to attribute this to valuation at time of purchase, though my data doesn't support that as being a consistent indicator. (Chuck does have a hammer, and though it is a wonderful hammer, there are times when he really should use a wrench.)"

Now I want it to be clear, that I took no offense from the above comment, or any of the other comments that were posted in the article. However, I did feel that the comment represented several assumptions that also led to erroneous conclusions that I believe were also made in the body of the article.

First and foremost, was the statement "the most interesting thing to emerge out of the data was how large the range was of total return in a group of stocks that are perceived by many as having very similar characteristics." (Emphasis added mine).

From my perspective, the only things that the 13 stocks discussed in the article really had in common was that they all paid a dividend, and that they were all Dividend Aristocrats. Other than that, I intend to demonstrate that these 13 companies are a very diverse group, and as such, not really similar at all.

Additionally, I believe the reference: "Chuck's approach seems to be to attribute this to valuation at time of purchase, though my data doesn't support that as being a consistent indicator" is in error on two counts. First of all, my approach does attribute valuation as a major source; however, that is only a part of my "approach." As I indicated earlier, the earnings growth (and/or cash flow growth) achievements of each company is actually a more important component of my approach, and to the generation of total return in the long run.

Second, as I intend to demonstrate with this article, my toolbox does contain "a wonderful hammer," but it also contains many other useful tools as well - including "a wrench." But most importantly, when I go about the job of analyzing common stocks, I am careful to utilize all of the tools at my disposal. As I often say, any job is easier when you have the proper tools.

The Devil is in the Generalities

I've always taken exception to the adage that "the devil is in the details," especially when dealing with common stock investments. In my opinion, the devil is in the generalities and the angels are in the details. The reason I feel this way is because over-generalizing a grouping of stocks can lead to drawing false conclusions based on erroneous original assumptions.

To me, the major erroneous original assumption with Psycho Analyst's article is the idea that the 13 companies featured possess "similar characteristics." In truth and fact, these 13 companies represent a very diverse set with significantly different individual characteristics. To illustrate my point, I offer the following excerpt from a previous article I wrote titled "Constructing and Designing The Stock Portfolio That's Just Right For You: Part 1" where I presented Peter Lynch's 6 primary categories of stocks. Therefore, I suggest that the 13 stocks referenced in Psycho Analyst's article represent apples-to- oranges comparisons because they represent different categories of stocks that fall into Peter Lynch's first 4 categories:

"Six Primary Categories, According To Peter Lynch

In his best-selling book "One Up On Wall Street" Peter Lynch presented six general categories of stocks that investors can choose from: Slow Growers, Stalwarts, Fast Growers, Cyclicals, Asset Plays, and Turnarounds. Although I believe that these six general categories provide great insight into the types of common stocks generally available for investors to choose from, some of these categories can be further broken down. For example, we could add moderate growth to slow growth, and very fast growth to fast growth, etc. Therefore, I feel it's important that the reader understands that there can be more specific subcategories beyond the general categories discussed by Peter Lynch or this article."

Moreover, considering that these 13 companies fall into significantly different categories, this also led to what I consider additional original erroneous assumptions. For example, in the third bullet point of the summary of Psycho Analyst's article, a thesis was presented suggesting that lower yielding stocks produce significantly higher total returns. As a general rule, there is a level of truth behind that assumption, but I will later argue that this truth only applies when the primary sources of return, (valuation and earnings growth) are examined and included. I don't believe those primary sources of total return were properly evaluated.

"Summary

We took the top 10 stocks from the Dividend Growth 50 and combined them with three other top performers from the Dividend Aristocrat list and arranged them by starting yield.

Then, we plotted their dividend return, share appreciation, and total return with dividends included over two different periods between the beginning of 1998 and the present.

The total return of the lowest-yielding stocks greatly exceeded that of the highest-yielding stocks, sending a message to investors, making investing decisions based solely on current yield."

Measuring Performance Void of the Sources of Return

As I previously stated, I consider Psycho Analyst's article well-written and the facts accurately presented. However, I also believe that the overly-generalized nature of what was presented does not properly support the conclusions that were drawn. It is my contention that the problem lies not with what was presented. Instead, the problem lies with what important considerations were omitted. Stated more directly, I believe that vital details were left out, and when added, would lead to entirely different but also more relevant conclusions. Moreover, I believe that this is the true message that should be sent to investors.

However, before I present the important missing details, I offer the following excerpts from Psycho Analyst's article that established the theme, thesis and approach utilized. When I present a more detailed look at each of the "Survival Bias 13," I will utilize the same time frame. However, my more detailed analysis will be offered to more clearly illustrate where and how the long-term total returns came from and were generated. My objective is to illustrate that measuring performance without due consideration of the primary sources of return (valuation and earnings growth) is a job half done:

"There has been a lot of debate about the value that dividends bring to long-term investing results. At one extreme, there are those investors who focus entirely on the income their stocks produce and how quickly that income grows. At the other are those who argue that wise retirees should care more about how much their total investment ends up being worth as shares can always be sold to provide needed income.

To get a better idea of how investing for dividend yield really performs over time compared to investing for total return, I decided to examine the actual performance of a group of actual stocks. To make the results relevant for dividend growth-focused investors, I decided to see how investing based on yield affected the returns of a highly select group of dividend growth stocks."

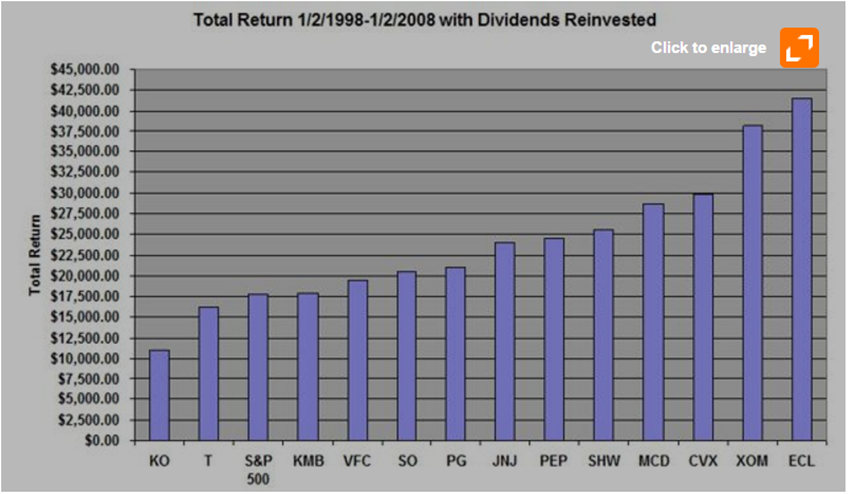

"Why I Choose To Track Performance From The Beginning Of 1998 To The Beginning Of 2008

I chose to examine how these stocks, which I will call the "Survival Bias 13" performed over the decade extending from 1/2/1998 through 1/2/2008. This period has some interesting parallels with the present. It began as the bull market of the 1990s was drawing to a close. This was followed by a significant three-year market decline followed by a strong recovery. The period ends at a point in the business cycle very much like where we find ourselves today: a point where the market had just begun to retreat from an all-time high but had not yet entered the profound decline of the Great Recession."

The Angels Are In the Details

What follows is a detailed analysis of the "Survival Bias 13" presented in the same order of lowest total return to highest total return over the time frame 1998-2008. I have utilized the scrolling feature of F.A.S.T. Graphs™ in order to focus on this specific time frame and illustrate the importance of valuation and earnings growth (and/or cash flow growth) as the primary sources of return. With each example, I will provide brief commentary discussing the attributes of each example in order to point out what I consider the fallacies of the generalized presentation and calculations presented in Psycho Analyst's article.

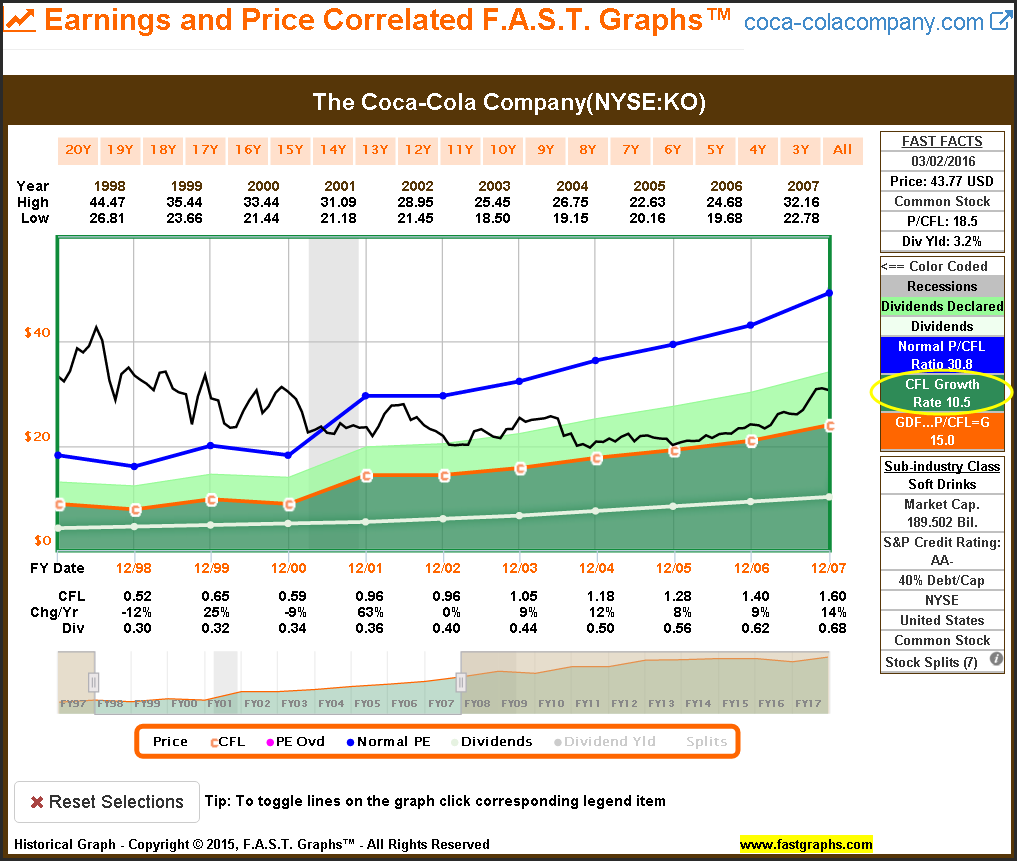

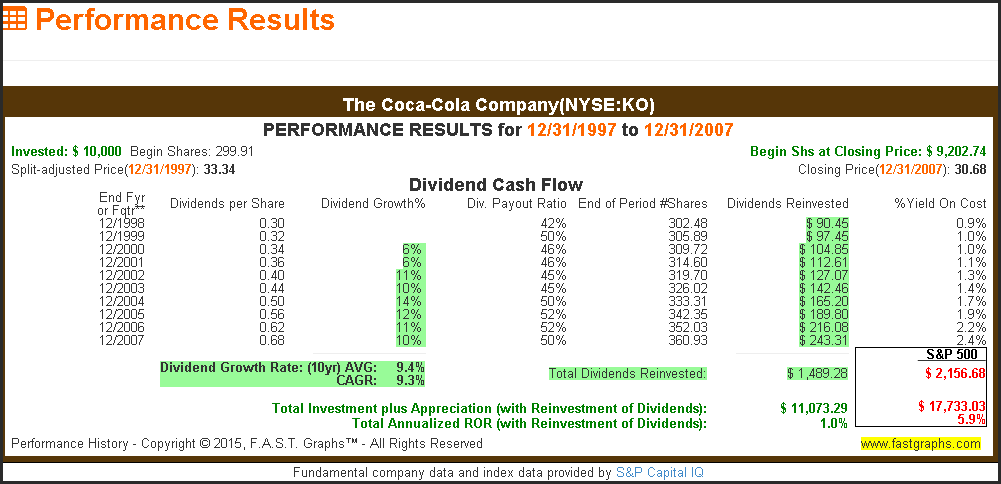

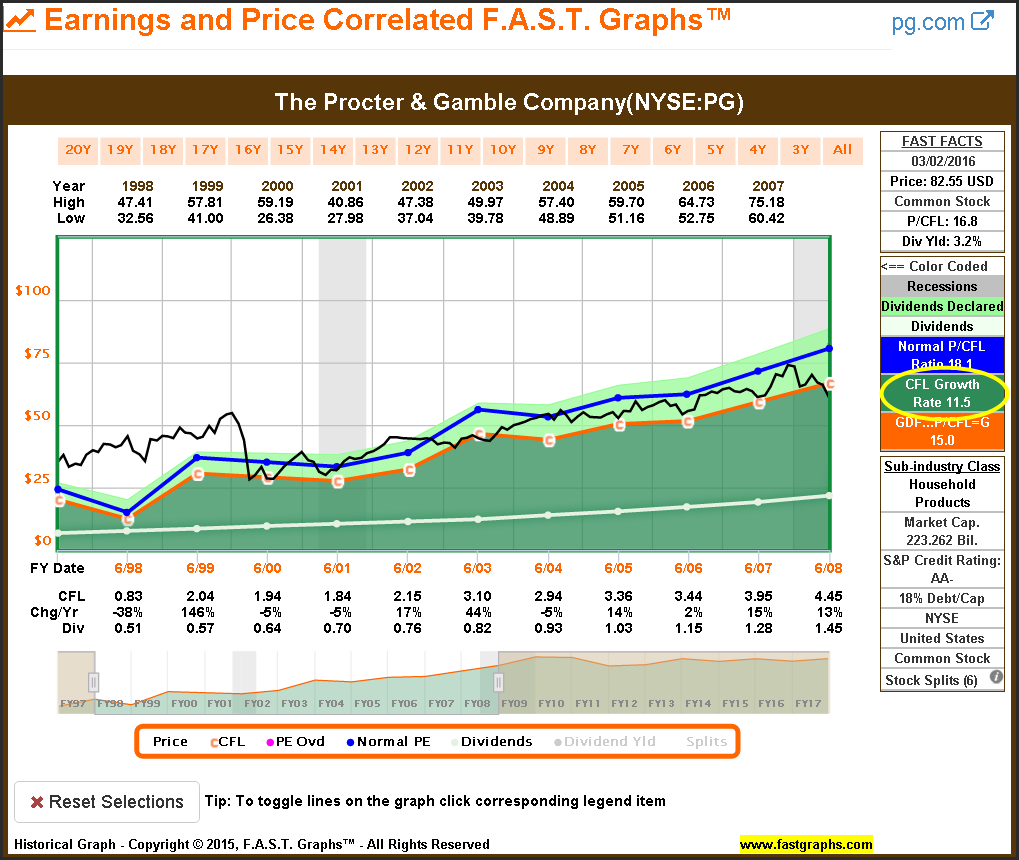

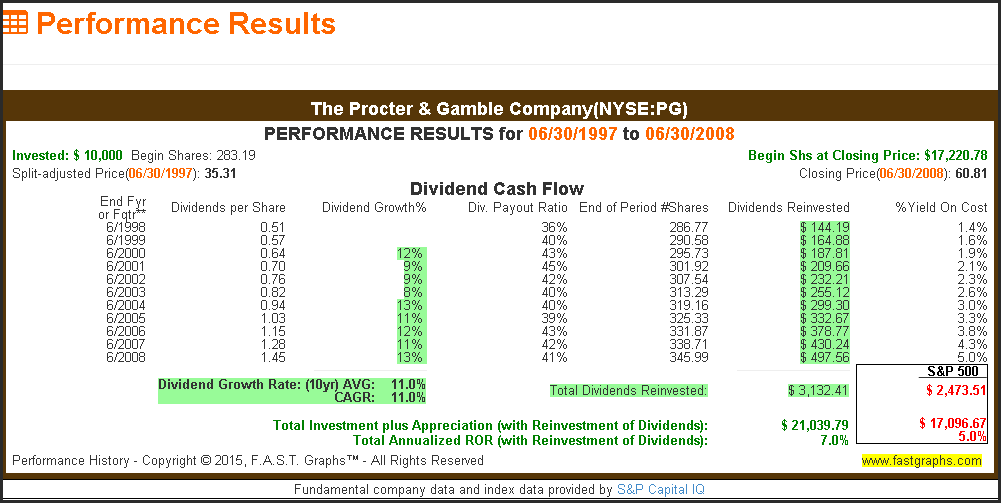

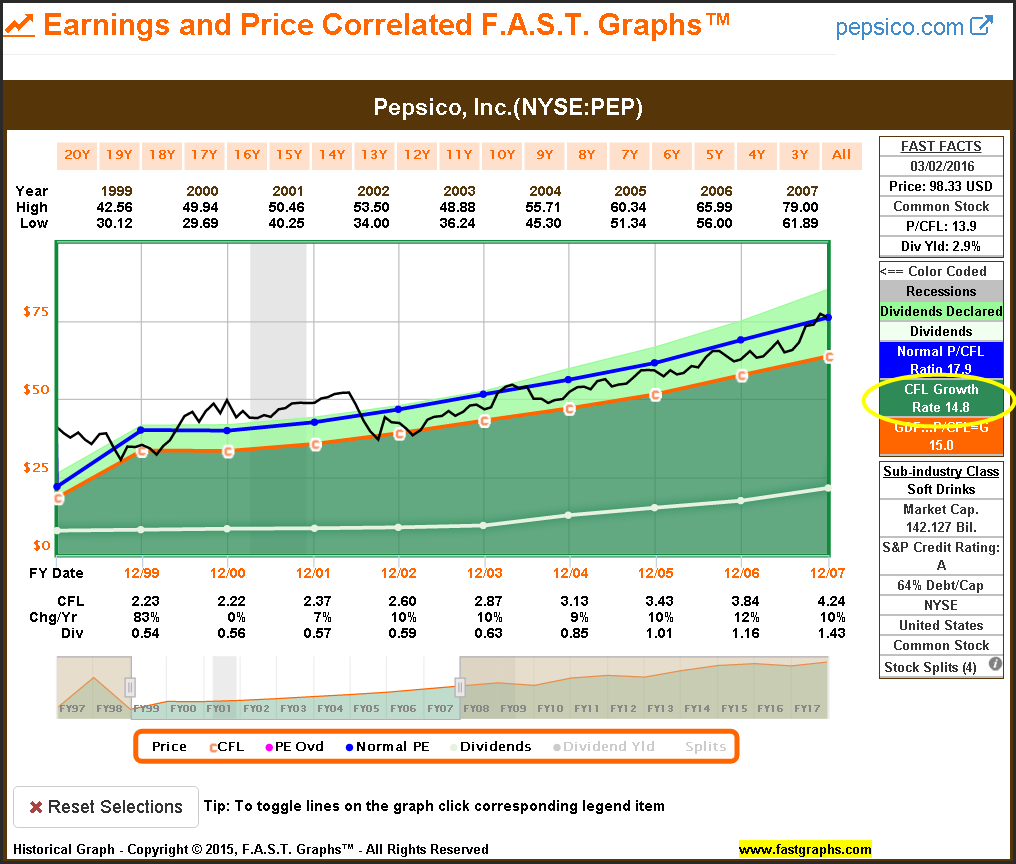

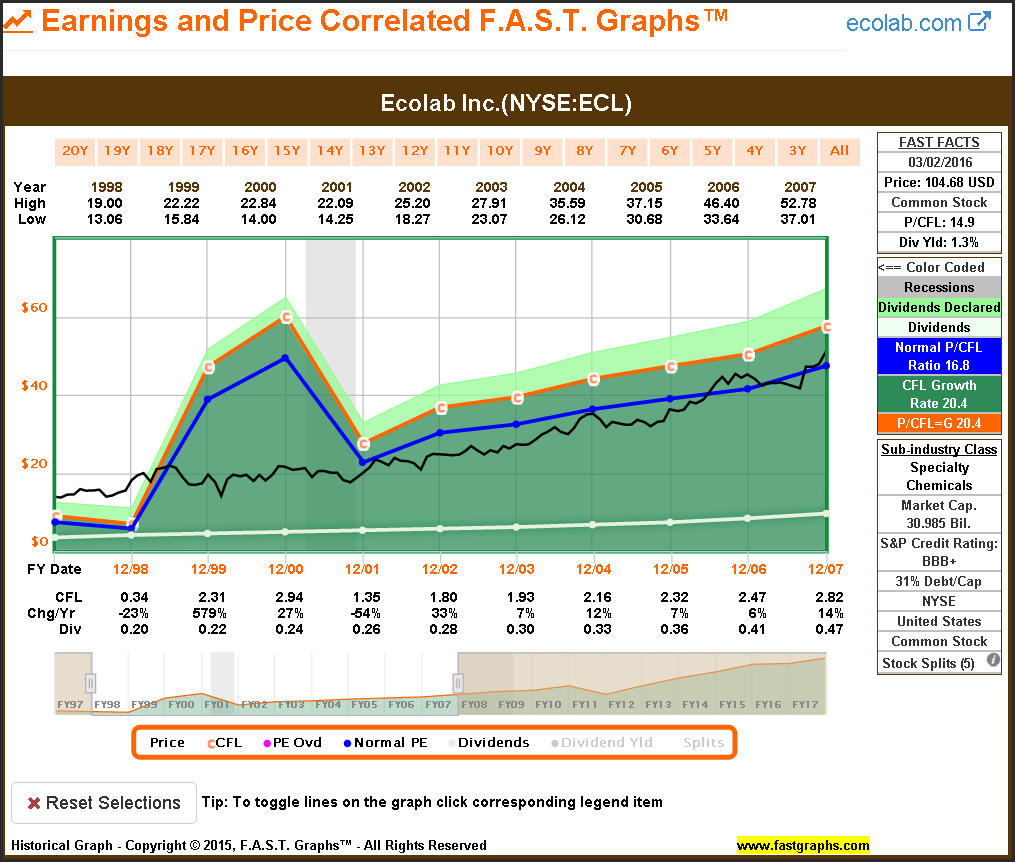

For most of the examples I have provided an earnings and price correlated graph, and for a few of the examples I also include a cash flow and price correlated graph. The price and cash flow graph is more appropriate for companies with histories of commanding a premium P/E ratio. For those companies, I have found that cash flow is often a more relevant valuation metric. I have also included appropriate performance results on each company with dividends reinvested.

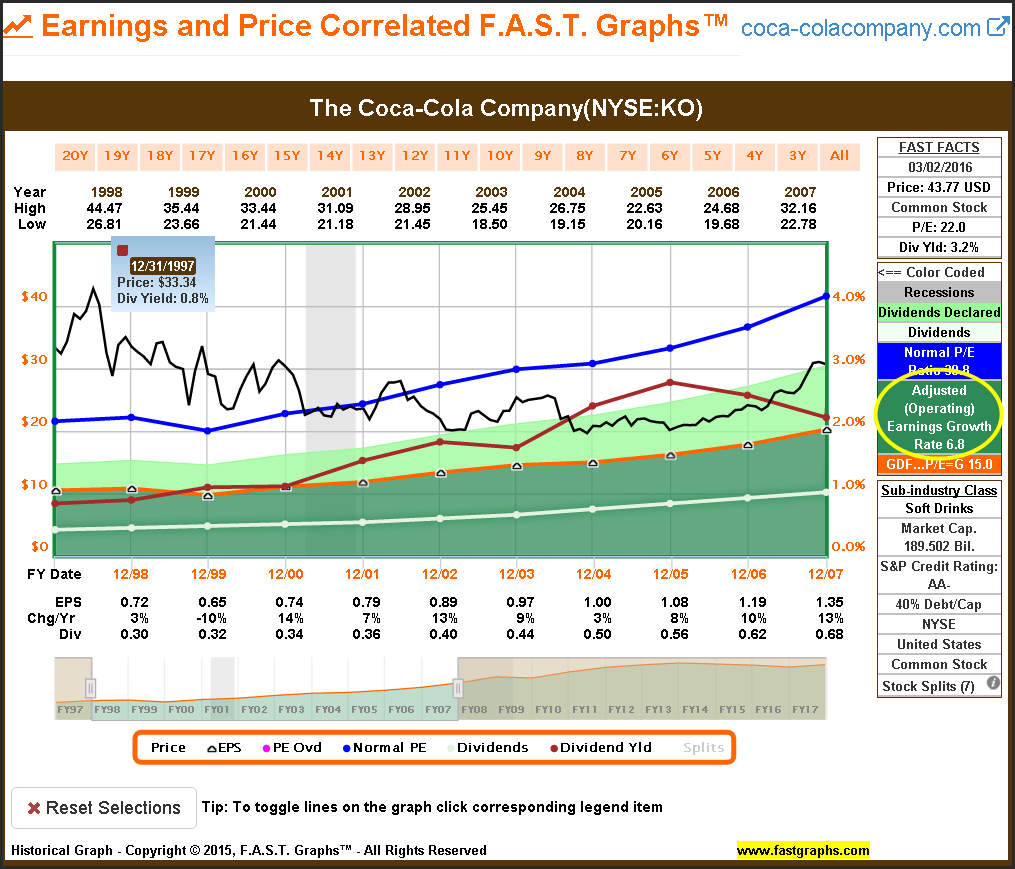

The Coca-Cola Company (NYSE:KO)

Coca-Cola was the worst performer of the "Survival Bias 13" and by a quick examination of valuation and earnings growth (and/or cash flow growth) over this time frame it is easy to see and understand why. Coca-Cola was significantly overvalued which greatly impacted its current yield and destroyed any of the benefit of its 6.8% annual earnings growth rate (Note: Psycho Analyst did acknowledge this in the original article). Notwithstanding that Coca-Cola is a Dividend Aristocrat; no rational valuation oriented dividend growth investor would have purchased Coca-Cola at these levels. Interestingly, the headwinds of overvaluation prove that a low starting dividend yield did not automatically imply strong long-term performance.

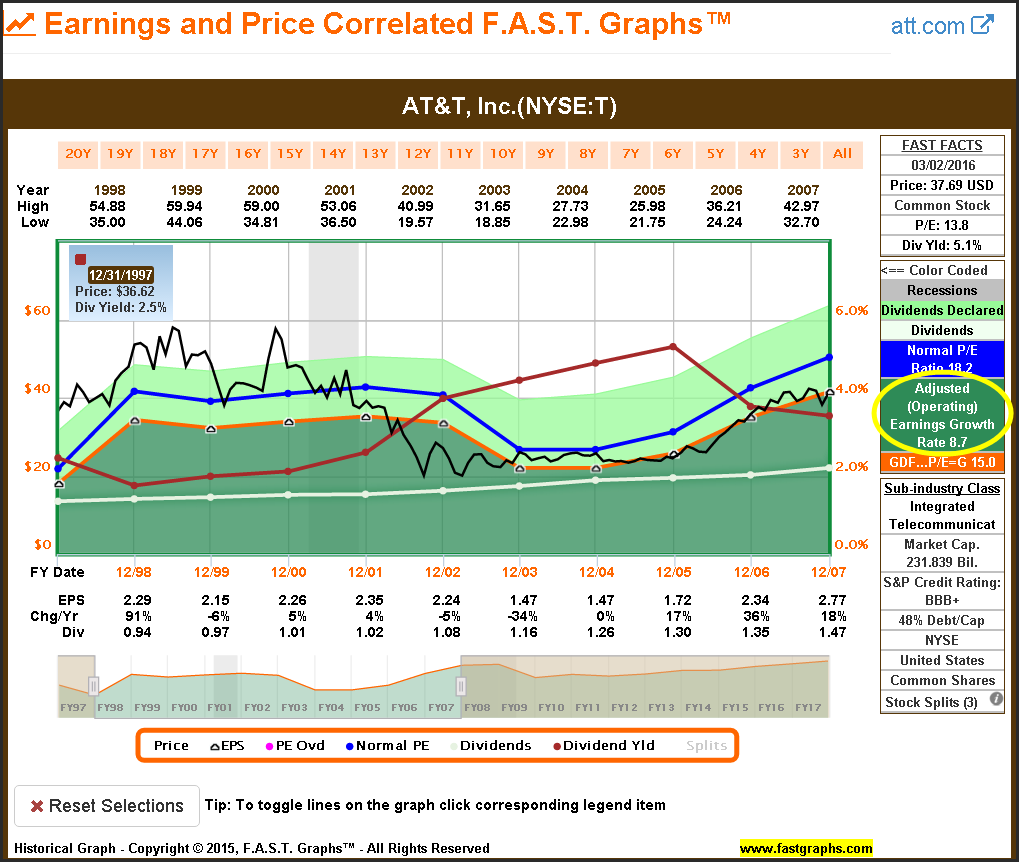

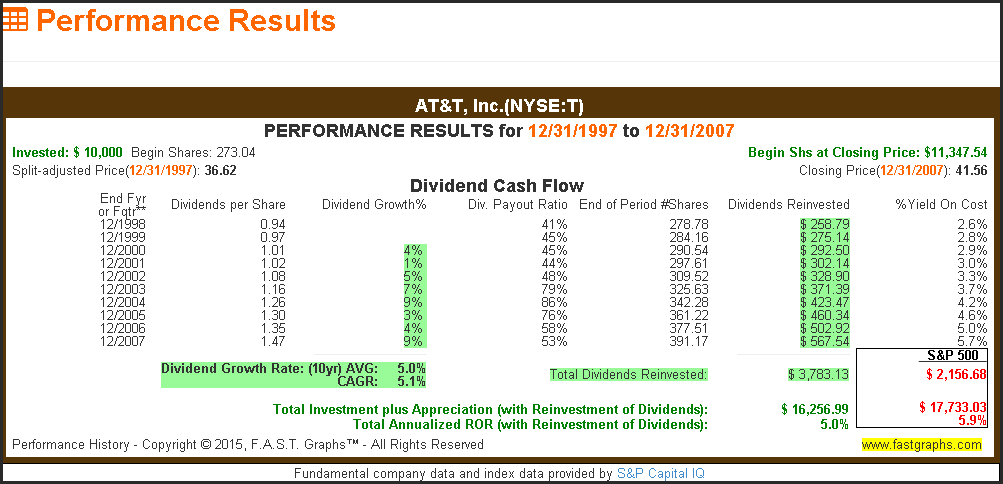

AT&T, Inc. (NYSE:T)

There are a couple of problems with including AT&T. First of all, this is actually two different companies being represented over this time frame. From 1998-2005 we have original AT&T founded in 1985. In 2005 SBC Communications, Inc. purchased the company but kept its iconic name and brand. Therefore, there is survival bias with this member of the "Survival Bias 13".

Although the starting yield was relatively high, AT&T was also overvalued and earnings growth was very inconsistent even though it averaged 8.7% annually. Earnings growth of 91% was powerful in 1998, but very flat and ultimately down over the next 5 or 6 years. Beginning overvaluation and erratic earnings growth were the primary sources of AT&T's poor performance over this time frame. No rational valuation-oriented dividend growth investor would have purchased AT&T at the beginning of 1998.

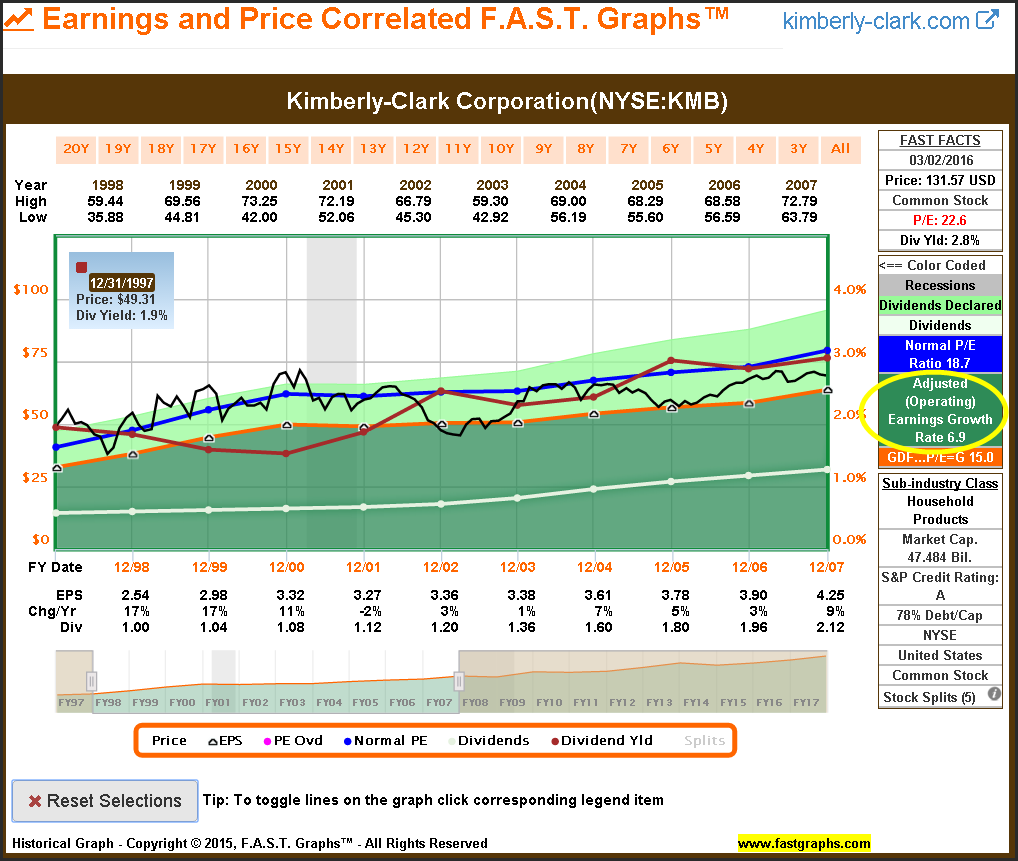

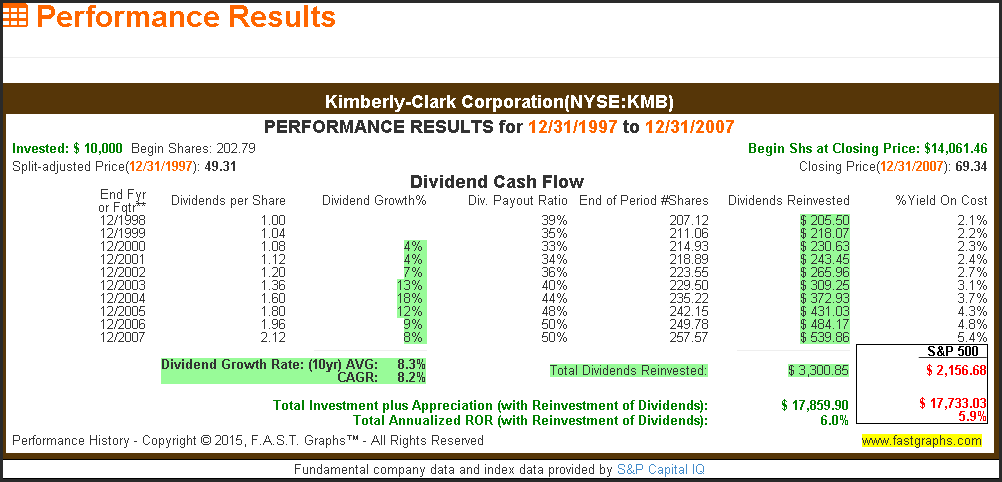

Kimberly-Clark Corporation (NYSE:KMB)

Kimberly-Clark was also overvalued at the beginning of 1998. Moreover, ending valuation was lower as the P/E ratio contracted from 22.6 at the beginning of 1998 to 16.3 by the end of 2007. Earnings growth was decent at 6.9% annually, but overvaluation leading to P/E ratio contraction greatly impacted the long-term total return.

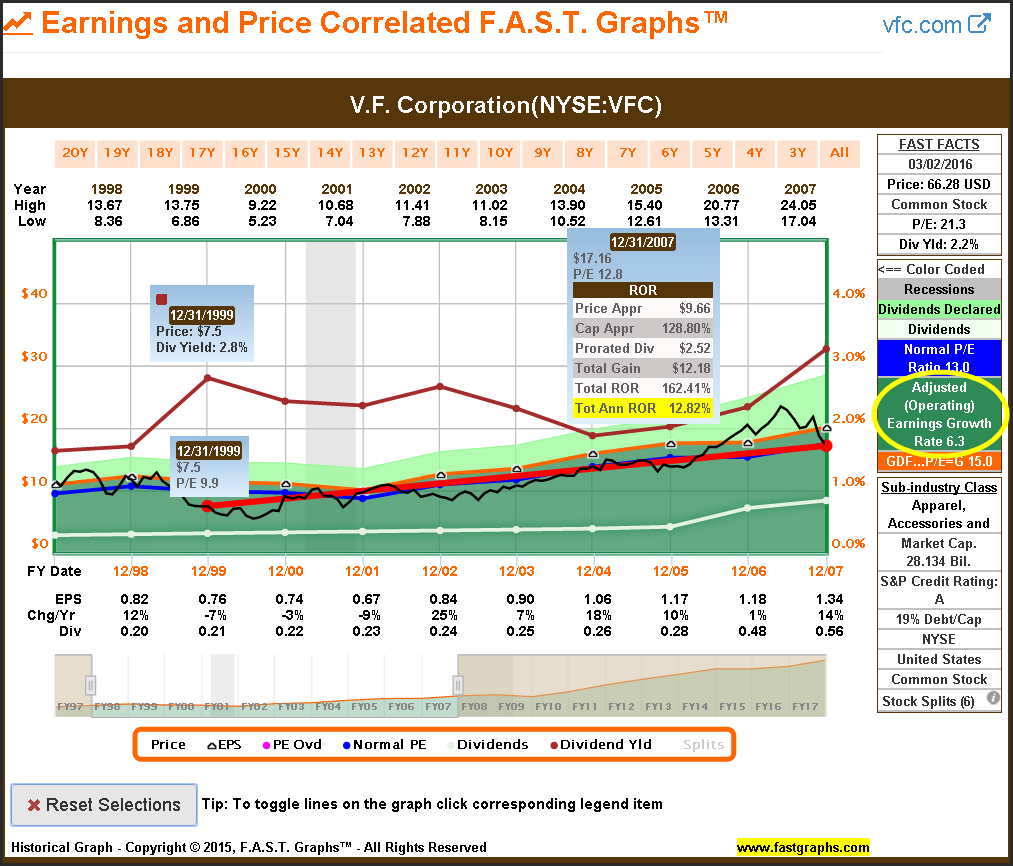

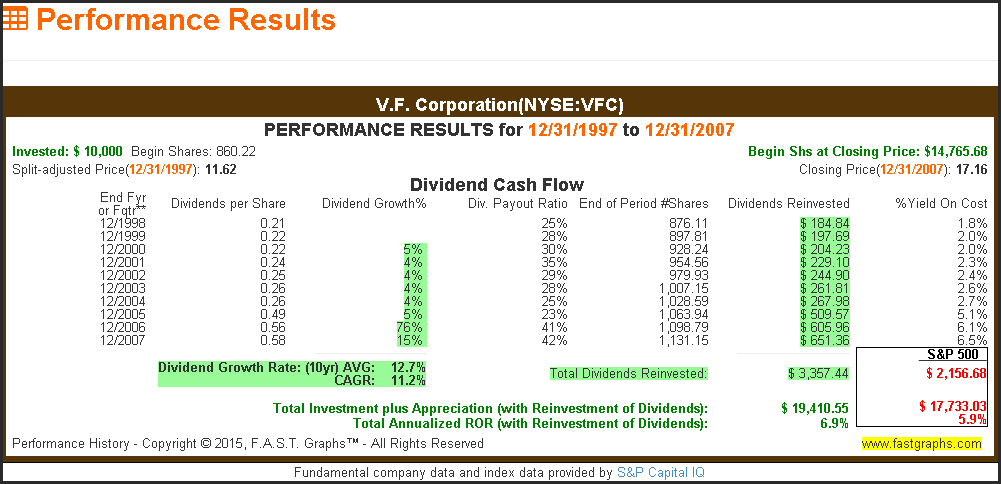

V.F. Corporation (NYSE:VFC)

V.F. Corporation was fairly valued at the beginning of 1998, and just slightly undervalued by the end of 2007. Consequently, the company's long-term total return over this time frame was reasonably consistent with its earnings growth achievement of 6.3% annually.

However, with this example, I added an additional calculation that illustrates the importance of valuation as it applies to long-term total returns. Rather than simply pick those companies that had the highest or lowest yields over this time frame in the general sense, I believe it is more relevant to measure the company's performance relative to its individual starting yields and growth rates. Therefore, the calculation on the graph (depicted by the bright red line), shows long-term performance when V.F. Corporation offered its highest relative dividend yield over this time frame.

Importantly, this was V.F. Corporation's highest year-end yield because it was also a period of time when valuation was low. Consequently, the total annual rate of return was approximately doubled and this calculation was generated without reinvesting dividends.

My point being that if you're going to analyze the ability of a company to generate long-term returns based on dividend yield, it is more relevant to conduct this exercise based on the various yields of the specific individual company. As stated in the title of this article, dividends don't drive return, they contribute to it.

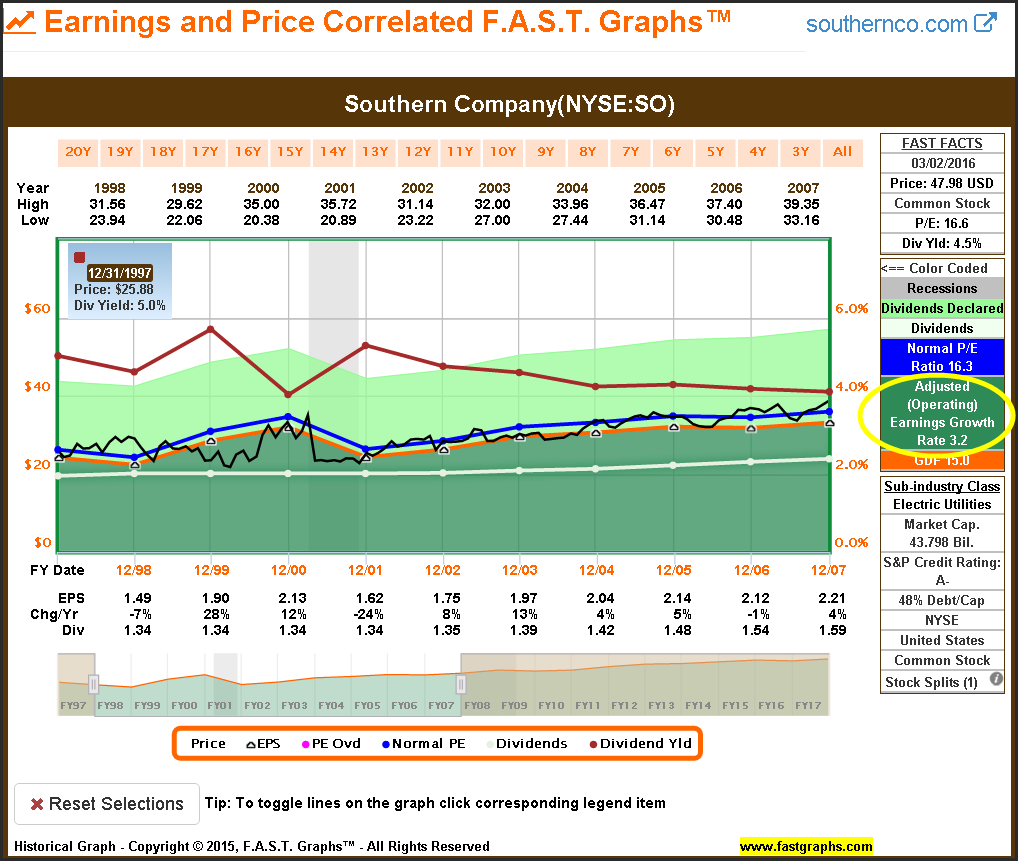

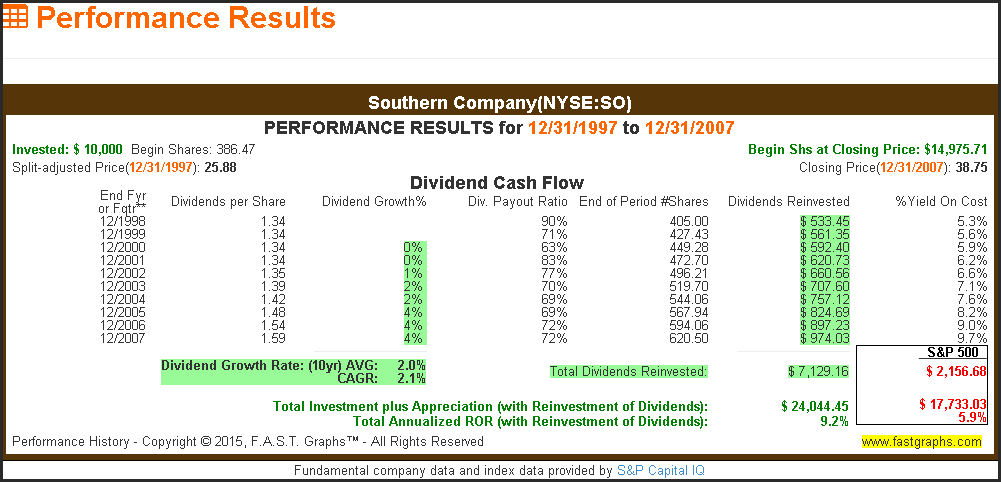

Southern Company (NYSE:SO)

Southern Company is a low growth regulated utility and therefore falls into the "Slow Growers" that Peter Lynch presented. Higher-yielding slow growers will rarely outperform on a total return basis. This category of company is best utilized by investors in need of a high current yield to live off of. You don't invest in utility stocks in order to generate high total returns. You invest in utility stocks for the consistent high dividend yields and safety they offer.

Nevertheless, Southern Company produced respectable results because valuation was reasonable at the beginning of 1998 and slightly elevated at the end of 2007. Dividends did make a significant contribution because the starting yield was high, but the annual dividend growth rate low and relative to its earnings growth rates.

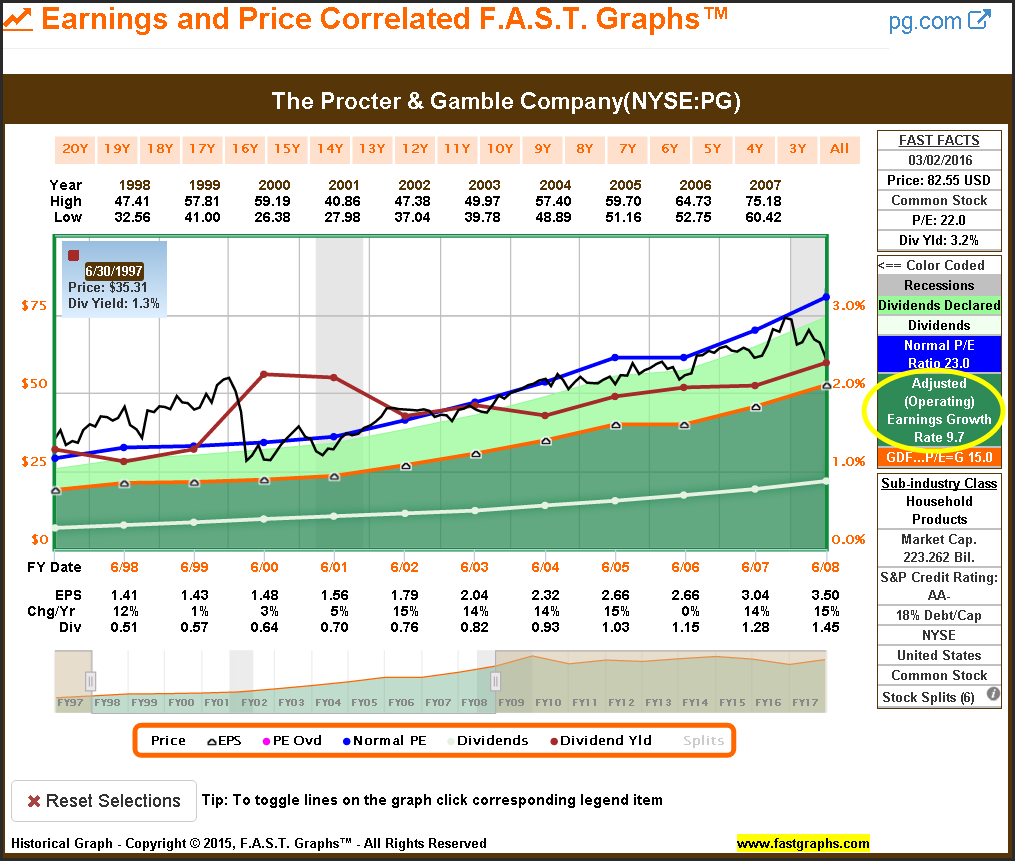

The Procter & Gamble Company (NYSE:PG)

Since Procter & Gamble has a June fiscal year end, therefore, my numbers will not perfectly match the numbers presented in Psycho Analyst's article. However, they are close enough to support my thesis. Procter & Gamble was overvalued at the beginning of fiscal 1998 and ended fiscal 2007 at a lower valuation (P/E contraction). Once again, no prudent value-oriented dividend growth investor would have invested in Procter & Gamble at the beginning of 1998.

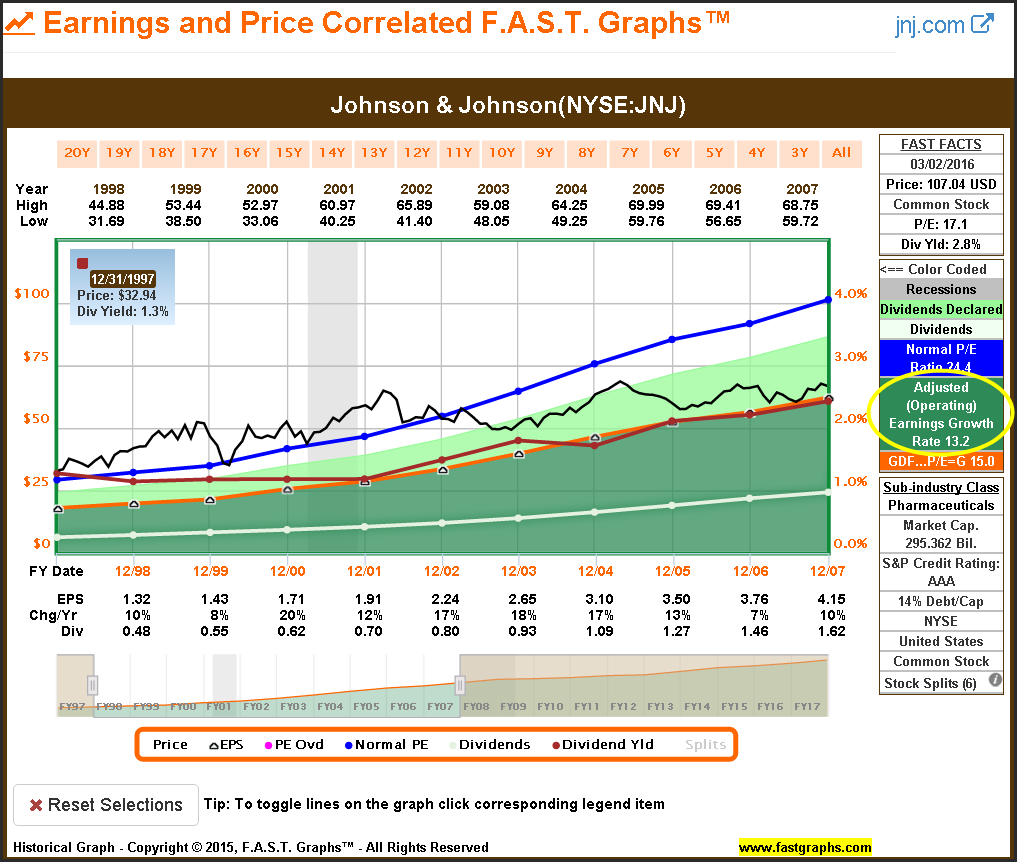

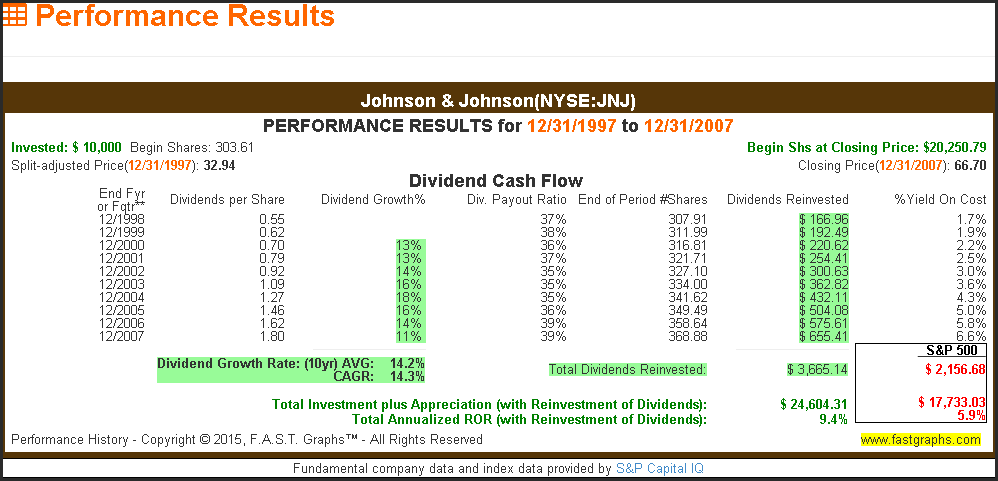

Johnson & Johnson (NYSE:JNJ)

Over the time frame 1998-2007 Johnson & Johnson produced superior and consistent earnings growth of 13.2% annually. However, the headwinds of beginning overvaluation greatly reduced the long-term total return it generated. The primary sources of return are valuation and earnings growth. In Johnson & Johnson's case, one out of two wasn't too bad.

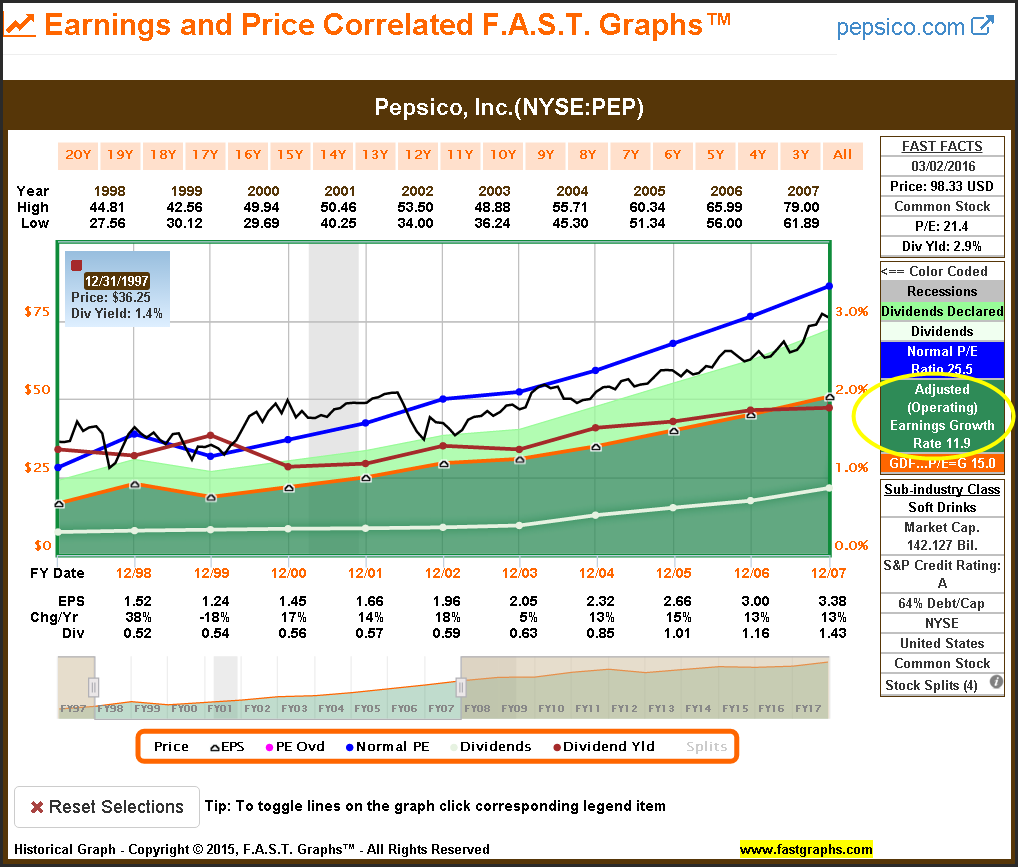

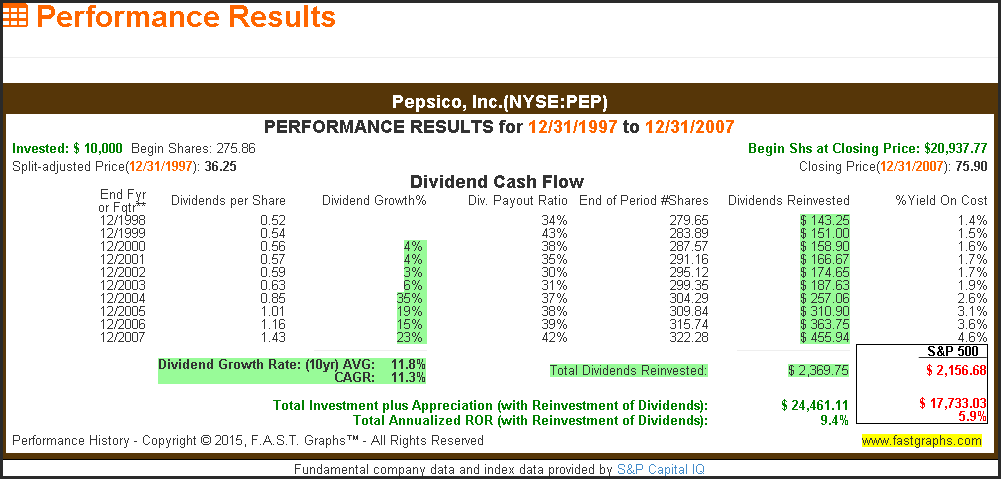

PepsiCo Inc. (NYSE:PEP)

Pepsi represents an example of a Peter Lynch stalwart that typically commands a premium valuation. However, beginning high valuation significantly reduced long-term total return in spite of its strong earnings growth rate of 11.9% annually.

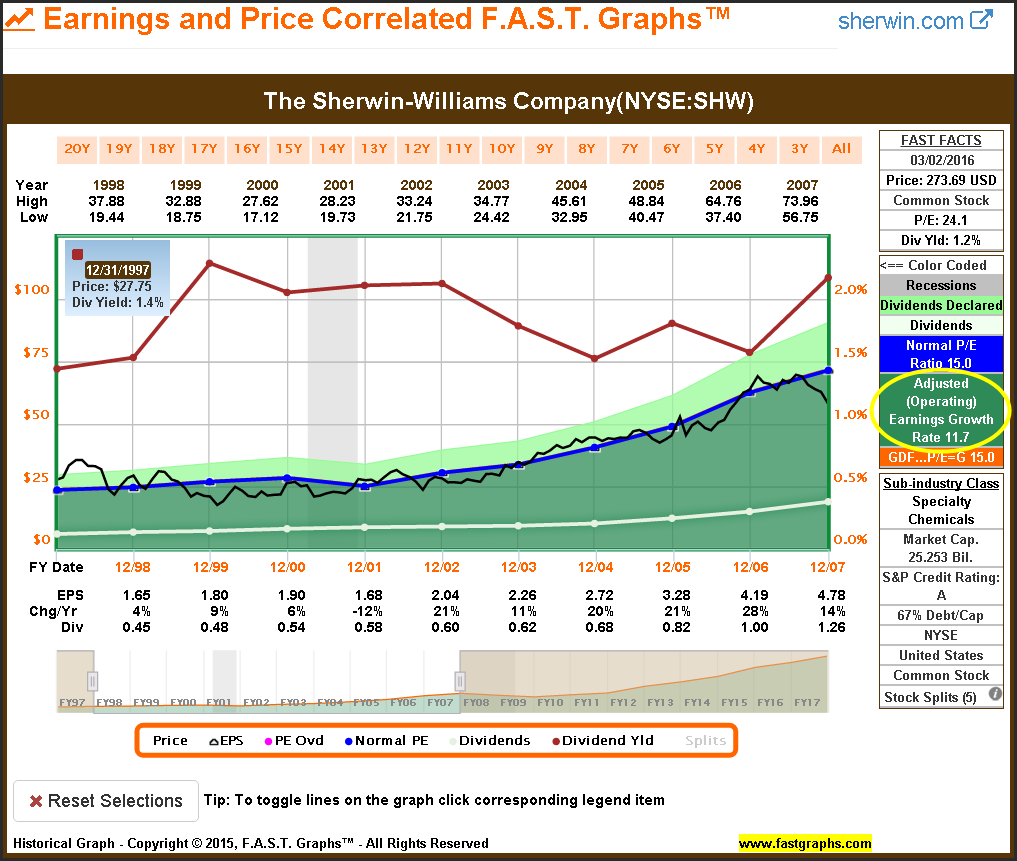

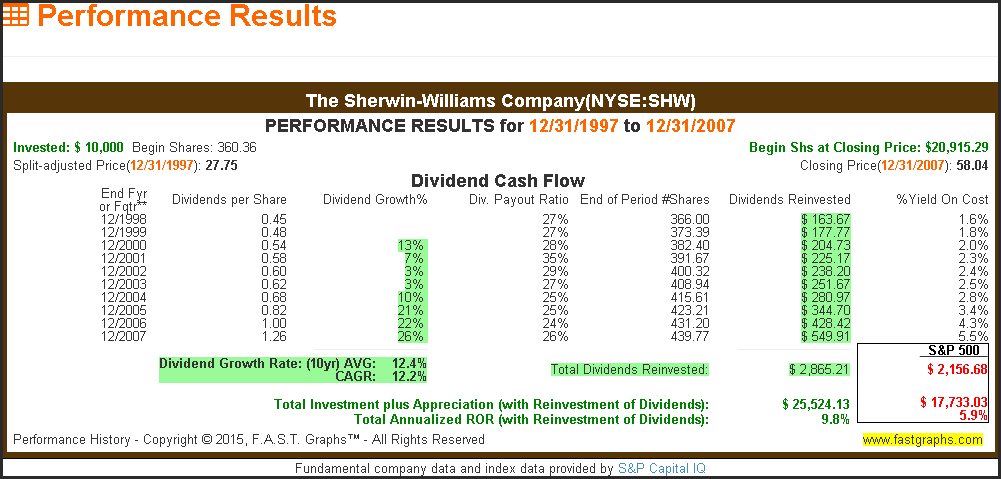

The Sherwin-Williams Company (NYSE:SHW)

Sherwin-Williams produced an above-average total return relative to the "Survivorship Bias 13" as a classic example of valuation and earnings growth being in relative alignment in both the beginning and at the end of the time period measured. Sherwin-Williams was just slightly overvalued at the beginning of 1998, and slightly undervalued by the end of 2007. Nevertheless, its strong and consistent earnings growth averaging 11.7% annually produced a strong and above-average total return. Valuation and earnings growth are the primary sources of long-term return.

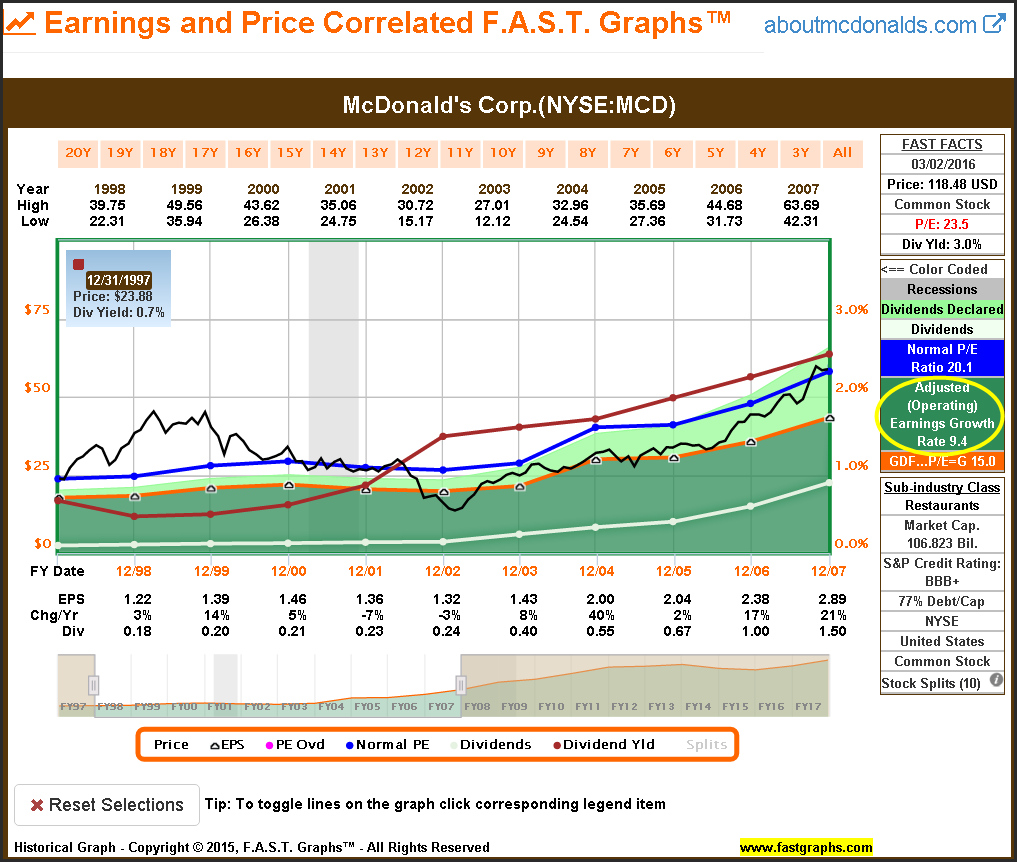

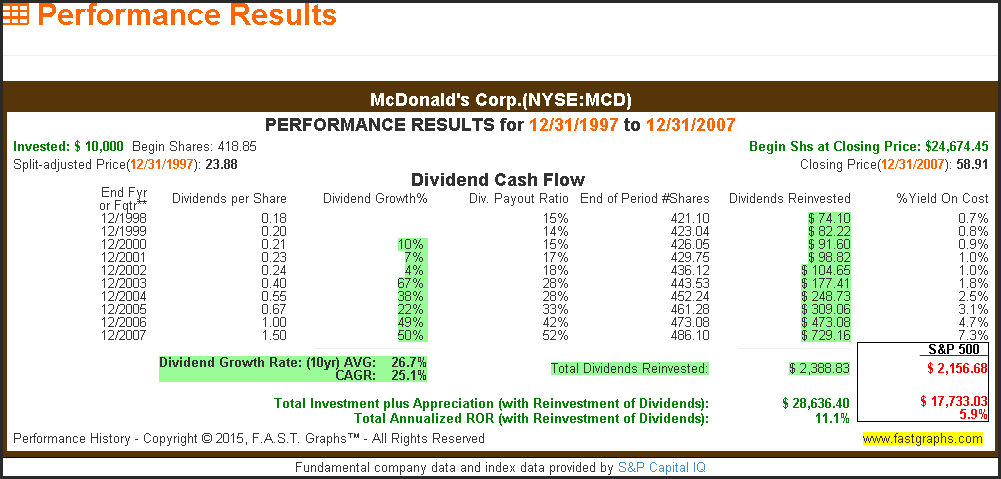

McDonald's Corp. (NYSE:MCD)

At the beginning of 1998 and again at the end of 2007, McDonald's was valued at its historical normal P/E ratio of 20.1. Consequently, the capital appreciation component of McDonald's total return exactly matched its earnings growth rate of 9.4% annually. Dividends reinvested contributed bringing in the total annualized rate of return to 11.1%. McDonald's results clearly illustrate the reality that earnings growth and valuation are the primary sources of long-term returns and also that dividends contribute.

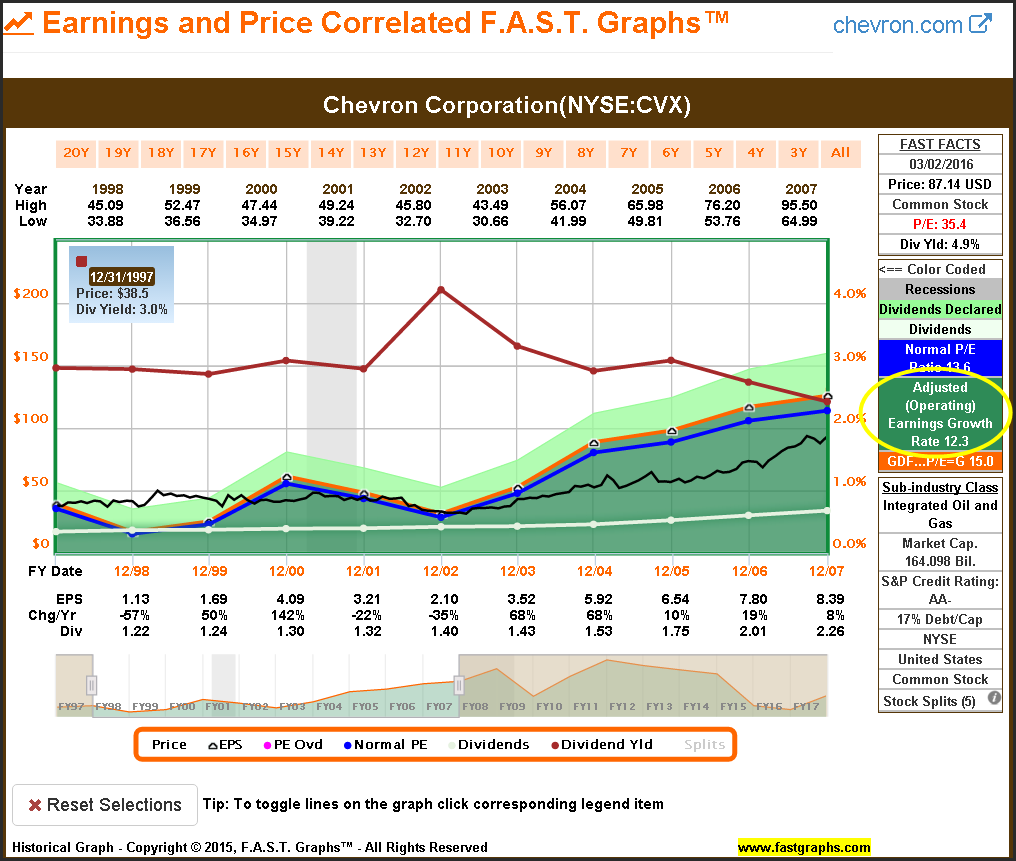

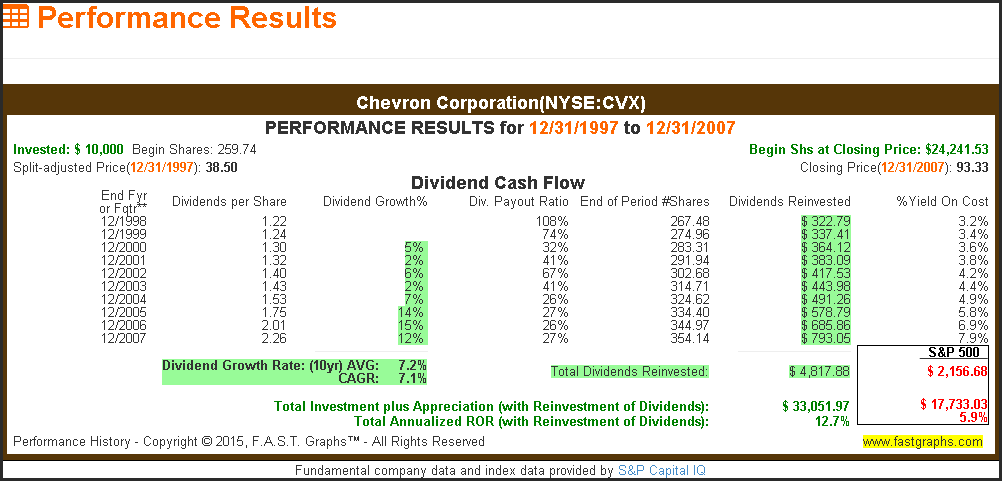

Chevron Corporation (NYSE:CVX)

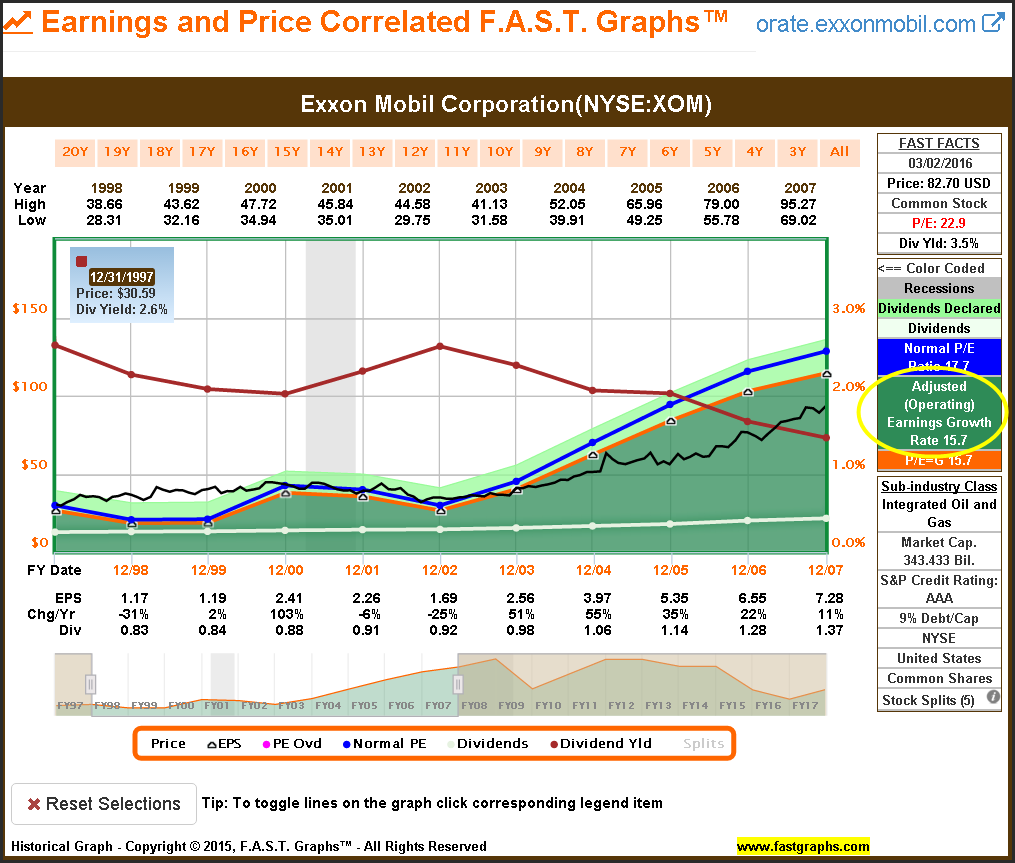

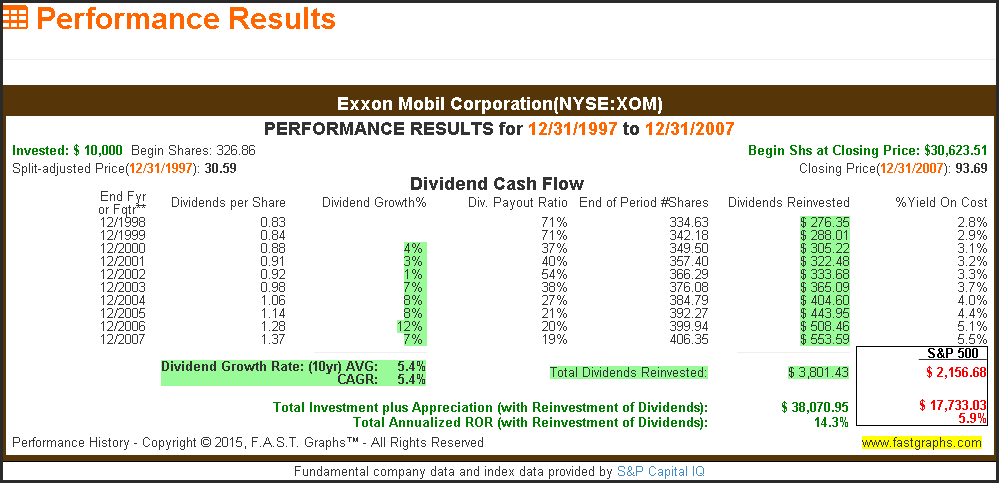

Both Chevron Corporation and Exxon Mobil Corporation produced strong earnings growth over the time frame 1998 to 2007. In both cases, beginning valuation was sound and ending valuation moderately undervalued. Consequently, both major integrated oil and gas producers produced strong total annual rates of return. Earnings growth and valuation are the primary sources of long-term returns.

Exxon Mobil Corp. (NYSE:XOM)

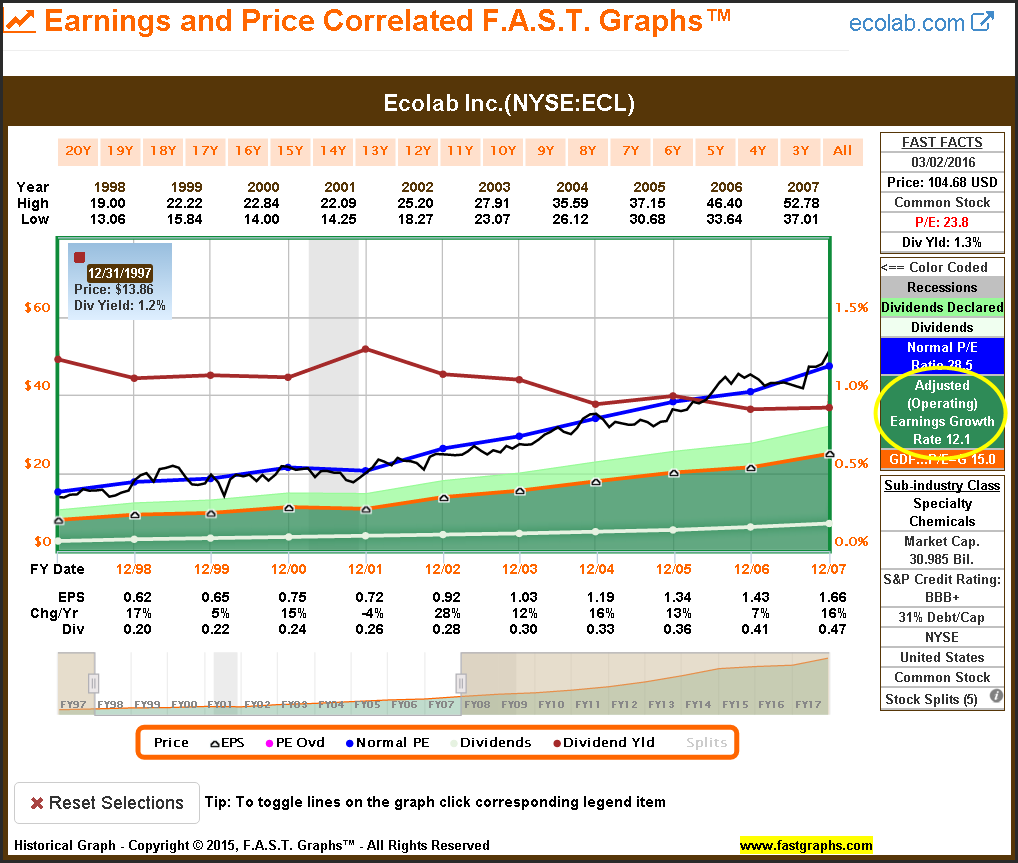

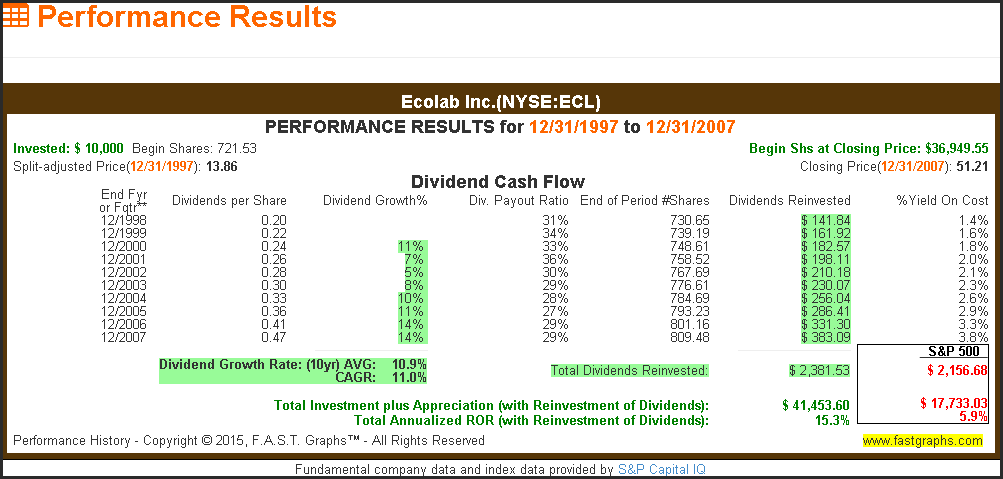

Ecolab Inc. (NYSE:ECL)

Ecolab is a classic example of a company that has historically commanded a premium valuation. Nevertheless, its status as the top performer is clearly established due to its double digit earnings growth rate of 12.1% annually. Based on its historical normal P/E ratio valuation, Ecolab started 1998 reasonably valued and ended just a little overvalued by the end of 2007. Superior total return is clearly functionally related to superior earnings growth (and/or cash flow growth) and not its low dividend yield.

Summary and Conclusions

As stated earlier, there is truth to the notion that lower dividend yielding stocks will generally generate a higher long-term total return. However, the reason is not because the dividend yield is low. Instead, the reason is typically because dividend growth companies that offer lower yields (and typically lower payout ratios) do so because they are still in their growth phases. Consequently, they pay lower dividends because they require capital to fund their growth. On the other hand, the above statement assumes calculating their dividend yields when valuation is sound.

Regarding the message that I want to send to investors, it is this. If you are in the accumulation phase with time to grow the common stock portion of your portfolios, then I would suggest that higher growth oriented investments make sense. This could include pure growth stocks that pay no dividends, or faster growing dividend growth stocks offering lower starting yields.

On the other hand, if you are already in retirement or near it, and your portfolio is large enough to provide enough income based purely on yield, then I would suggest investing in blue-chips that were fairly valued with higher current yields. The ideal situation for a retiree is when their portfolio provides enough income without having to harvest principle. It's also ideal when the income increases each year.

Choosing the most appropriate investments is not always about going after the highest total return, nor is it always about seeking the highest dividend yields. The most appropriate investments are the ones that meet each individual's needs, goals and objectives. However, regardless of which type of investor you are, it's important to understand where and how investment returns are generated.

Disclosure: Long KO,T,KMB,SO,PG,JNJ,CVX,PEP,MCD

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

Disclosure: I am/we are long KO,T,KMB,SO,PG,JNJ,PEP,CVX,MCD.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

ไม่มีความคิดเห็น:

แสดงความคิดเห็น